Getting a Mortgage in Spain as a Non-Resident: The 2026 Essential Guide

Owning a slice of the Spanish sun in 2026 is a rewarding lifestyle transition, yet the path to financing it has become a sophisticated strategic operation. Getting a mortgage in Spain as a non-resident involves more than just a bank application. It requires understanding a landscape where the 12-month Euribor reached 2.86% by May 2026.

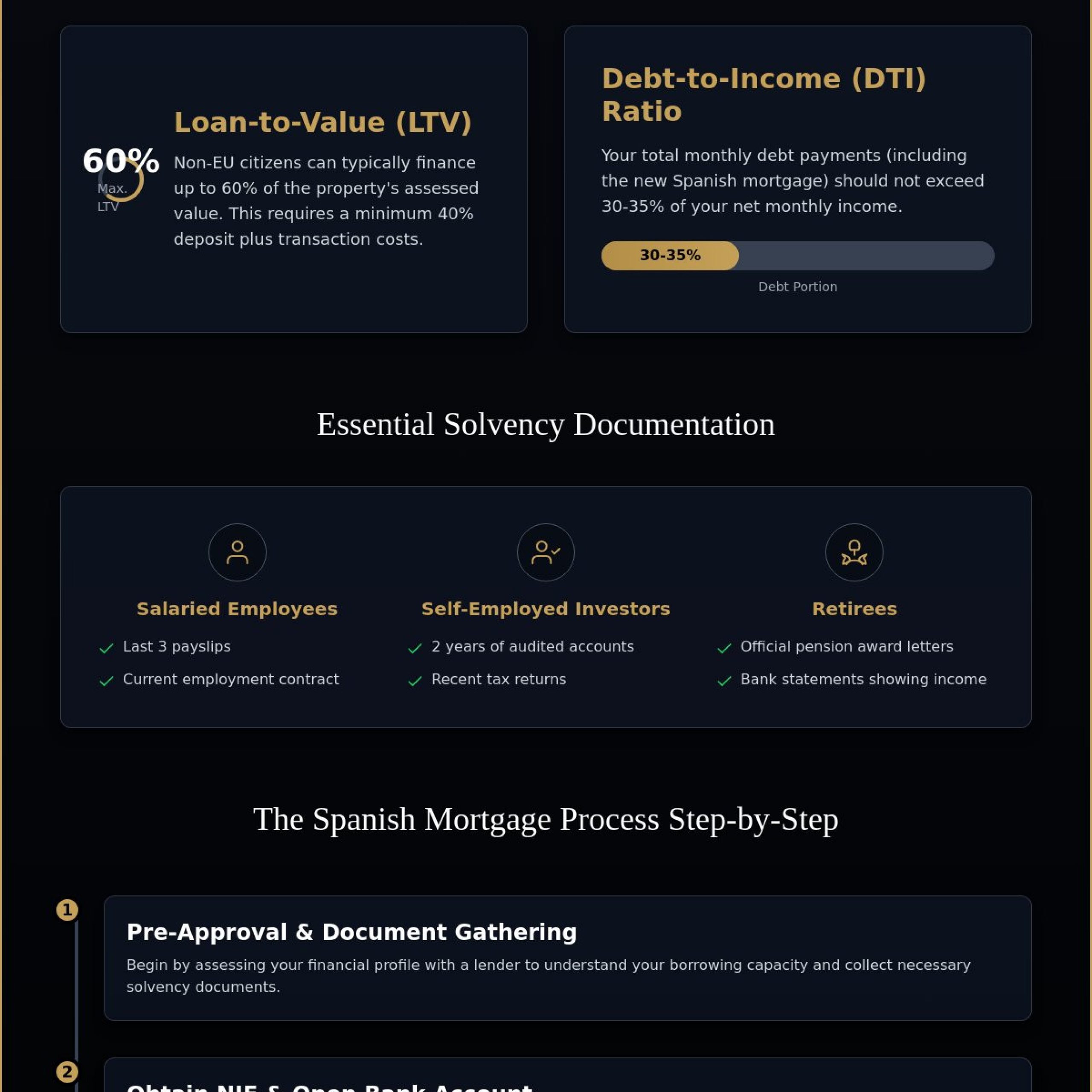

You likely feel the weight of the local bureaucracy, from the 60% loan-to-value limits for non-EU citizens to the complex coordination of legal deadlines. It’s natural to feel anxious about hidden fees or the strict 35% debt-to-income ratios that Spanish lenders now enforce.

This guide provides the professional assurance you need to master these international lending complexities and secure your investment with confidence. We’ll detail current borrowing limits, provide a verified document checklist, and outline a streamlined path from your initial pre-approval to the final signing at the notary.

Key Takeaways

- Gain a clear understanding of the 2026 economic landscape and how current interest rate benchmarks influence your borrowing capacity.

- Master the specific solvency standards and documentation required for getting a mortgage in Spain as a non-resident.

- Navigate the differences between fixed, variable, and mixed-rate structures to choose the most secure path for your lifestyle goals.

- Follow a streamlined timeline from your initial inquiry to the final notary signing, ensuring you stay ahead of critical legal deadlines.

- Learn how expert transaction management bridges the gap between international financial goals and local banking bureaucracy.

The Landscape of Getting a Mortgage in Spain as a Non-Resident in 2026

Securing a home in Spain is a dream shared by many global investors, but the technical reality of getting a mortgage in Spain as a non-resident requires a specific financial lens. In the eyes of Spanish banks, a non-resident is any individual who pays their primary income tax outside of Spanish territory. This definition is the cornerstone of your application and determines the specific lending criteria you must meet.

By 2026, the lending environment has matured significantly. Spanish institutions have embraced a digital-first approach that allows international buyers to manage applications from anywhere in the world. This technological shift has removed many of the traditional barriers that once made cross-border financing feel like an administrative hurdle, offering a more transparent experience for the modern investor.

Banks remain highly motivated to finance apartments and villas because these assets represent stable, high-value collateral in a desirable market. While the application process is now faster, the criteria for approval remain rigorous. Lenders focus on high-quality profiles to ensure long-term financial security for both the bank and the borrower.

Defining Non-Resident Status and Eligibility

The primary distinction for your application is the 183-day rule. If you spend fewer than 183 days per year in Spain, you are classified as a non-resident for tax purposes. This status dictates the specific loan products available to you, which often differ in terms of interest rates and maximum borrowing limits compared to resident loans.

Your country of residence also plays a vital role in bank risk assessments. Lenders evaluate the stability of your local economy and the ease of verifying your foreign income documents. Despite these technical checks, the allure of the Mediterranean lifestyle continues to drive a robust market for international buyers seeking a secure second home.

The 2026 Market Outlook for International Borrowers

Interest rate trends in 2026 reflect a period of stabilization following previous volatility. The 12-month Euribor, a critical benchmark for Spanish lending, stood at 2.25% in January 2026 before rising to 2.86% by May. These figures directly influence the daily pricing of both fixed and variable mortgage products available to non-residents.

EU-wide financial regulations have also standardized many aspects of the lending process. These rules provide increased transparency and protection for borrowers, ensuring that all fees and conditions are clearly disclosed before you sign. This regulatory framework builds immediate trust and simplifies the comparison of different bank offers across the Spanish market.

The average non-resident mortgage term in 2026 typically spans up to 25 years, provided the loan is fully repaid by the time the borrower reaches age 75.

Financial Requirements and Documentation for Foreign Borrowers

Spanish financial institutions prioritize stability and clear, declarative reporting when evaluating your application. While the process of getting a mortgage in Spain as a non-resident is structured, you must demonstrate a high level of solvency through verified documentation from your home country.

Two logistical pillars support every application: the NIE (Número de Identidad de Extranjero) and a Spanish bank account. Your NIE is the mandatory identification number for all financial and legal transactions in Spain. You’ll also need a local bank account to service the loan, as lenders require direct debits for monthly repayments and associated property taxes.

Lenders insist on a local account to ensure they have immediate access to funds for the monthly mortgage installment. This account also serves as the hub for your property-related expenses, including insurance premiums and community fees. Having these elements in place before starting your search demonstrates a high level of preparation to potential sellers.

Proving Income and Solvency Abroad

Banks apply a strict debt-to-income (DTI) ratio, typically ensuring that your total monthly debt obligations don’t exceed 30% to 35% of your net income. This calculation includes your existing mortgage or rent abroad, personal loans, and the projected Spanish mortgage payment.

Salaried employees should provide their last three payslips and a current employment contract to establish a steady income stream. For self-employed investors, banks often require two years of audited accounts or tax returns to verify business profitability. If you’re a retiree, lenders view international pension income favorably, provided it’s documented with official pension award letters and bank statements.

The Essential Non-Resident Document Checklist

Preparation is the key to a smooth approval process. Before approaching a lender, ensure you have gathered mandatory items such as your passport, NIE certificate, and your last three to six months of personal bank statements showing both income and regular expenses.

Understanding these Spanish bank mortgage requirements helps you present a professional profile that builds immediate trust with credit committees. You’ll also need tax returns from your country of residence for the last two financial years and a comprehensive credit report from a recognized agency in your home jurisdiction.

Providing translated and legalized documents where necessary ensures your application moves through the system without administrative delays. If the paperwork feels overwhelming, our team can help you organize your file to meet the highest banking standards. You can learn more about our approach to dedicated client support and expert transaction management.

Comparing Mortgage Types and Loan-to-Value (LTV) Ratios

Getting a mortgage in Spain as a non-resident requires a larger upfront capital commitment than a local resident application. Banks view international loans through a lens of increased risk because your primary income and assets are located outside Spanish jurisdiction. This risk assessment directly impacts the amount a lender is willing to advance against the property.

By 2026, the distinction between EU and non-EU borrowers has become more pronounced in bank policies. While EU citizens may still access up to 70% financing, those from the UK, USA, or other non-EU nations typically find Loan-to-Value (LTV) ratios capped at 50% to 60%. This conservative approach ensures the bank maintains a significant equity buffer in the asset.

Transparency is the foundation of a successful investment. Beyond the interest rate, you must evaluate opening commissions and the cost of bundled products like life or home insurance. These “vinculaciones” are often required to unlock the most competitive rates, and their long-term costs should be factored into your overall financial strategy.

Understanding LTV Limits for Second Homes

It is a common misconception that the LTV is based solely on the purchase price. In reality, Spanish lenders use the lower of two figures: the agreed purchase price or the bank’s official appraisal value (tasación). If the appraisal is lower than the price you’re paying, your required deposit will increase to cover the difference.

Strategic buyers should also prepare for the “acquisition costs” that a mortgage does not cover. You will need roughly 12% to 15% of the property value in cash to handle Transfer Tax (ITP), notary fees, and land registry charges. This capital must be readily available in your Spanish account well before the completion date.

Fixed vs. Variable: Choosing the Right 2026 Strategy

In the 2026 market, fixed-rate mortgages provide essential security for non-resident buyers. With rates for non-EU applicants ranging between 4.3% and 5.2% for 20-year terms, these products protect your lifestyle from future fluctuations in the European Central Bank’s policies. You’ll know exactly what your Mediterranean retreat costs every month.

Variable rates offer a different kind of advantage for those planning a shorter investment horizon or early repayment. These loans are tied to the 12-month Euribor, which stood at 2.86% in May 2026, plus a bank spread of 1.5% to 2.5%. This structure allows you to benefit if rates drop, though it requires a higher tolerance for monthly payment changes.

Mixed mortgages have become the preferred “middle ground” for modern investors. These allow you to enjoy a fixed rate for the initial 3 to 10 years, providing stability during the early stages of ownership. Afterward, the loan transitions to a variable rate, offering a balanced approach to long-term financial planning.

A Step-by-Step Guide to the Spanish Mortgage Process

Getting a mortgage in Spain as a non-resident has evolved into a methodical, 8 to 12-week journey. Modern digital portals now allow you to manage much of the initial document submission and coordination remotely. This efficiency ensures your financial timeline aligns perfectly with the property buying process in Spain.

The transition from a global investor to a Spanish homeowner is now more transparent than ever. By utilizing digital signatures and encrypted document portals, banks have removed many of the traditional geographic barriers. You can now track your application’s progress in real-time while you’re still in your home country.

This streamlined approach requires disciplined coordination between your financial advisor, the bank, and your legal representative. Each phase of the process is designed to protect your interests and ensure the long-term security of your investment. Following these steps carefully will lead to a successful completion at the notary.

Pre-Approval and Property Selection

Securing an “Approval in Principle” is your first essential milestone. This document confirms your borrowing capacity before you begin viewing homes. It gives you the quiet confidence to negotiate with sellers, showing them you’re a serious and qualified buyer in a competitive market.

Once you’ve found the right home, you’ll sign the “Arras” or deposit contract. This private agreement reserves the property and establishes the completion deadline. Your bank will require a copy of this signed contract to transition from a general pre-approval to a specific loan offer for that specific asset.

Appraisal, Notary, and Completion

The bank will then instruct an official appraisal, known as a “Tasación.” This valuation is a critical safeguard for both you and the lender. It ensures the property’s market worth supports the purchase price and determines the final loan amount the bank’s credit committee will release.

After the valuation, the bank issues the FEIN (Ficha Europea de Información Normalizada). Under Spanish law, you must wait through a mandatory 10-day reflection period after receiving this binding offer. This “cooling off” period is designed to ensure you’ve fully reviewed all terms before the final commitment.

The journey concludes at the Notary’s office where you’ll sign the purchase deed and the mortgage deed (Escritura). The Notary acts as an impartial official, verifying that you understand every clause and that the bank has met all legal requirements. Once signed, the mortgage is officially registered at the Land Registry to secure the title.

Ready to begin your journey toward owning a Mediterranean retreat? You can contact our expert team to secure your pre-approval today.

The Role of Professional Facilitation in Your Mortgage Journey

Getting a mortgage in Spain as a non-resident is a multi-faceted endeavor that extends beyond a simple bank approval. It requires the synchronized efforts of financial advisors, legal experts, and local specialists to ensure a seamless transition. By centralizing these moving parts, you transform a complex bureaucratic process into a manageable, stress-free experience.

A seasoned expert at KEYS property group acts as your dedicated transaction manager, bridging the gap between your international goals and the nuances of Spanish banking. This level of professional oversight ensures that every document is filed correctly and every deadline is met. You gain the peace of mind that comes from having a local advocate who understands the emotional and financial weight of your investment.

Local market intelligence is a powerful tool during bank negotiations. An experienced facilitator knows which lenders are currently favoring specific buyer profiles and can leverage this knowledge to secure more favorable terms. This proactive approach often results in better interest rates and reduced commission structures that might not be available to independent applicants.

Integrated Financial and Legal Support

Coordinating your legal assistance with your mortgage application is vital to preventing administrative delays. Your legal team can verify property encumbrances and outstanding debts long before the bank’s appraiser arrives on-site. This early intervention protects your deposit and ensures the asset is “clean” for financing.

Utilizing specialized currency exchange services can save you thousands of Euro on large international transfers. Traditional banks often charge high margins on foreign exchange, but a professional facilitator can connect you with competitive providers. These savings effectively offset a significant portion of your initial setup fees.

Post-Sale Management and Asset Care

The relationship doesn’t end once you’ve signed the deeds at the notary. Protecting your new investment requires ongoing care, especially when you’re residing abroad for most of the year. Comprehensive property maintenance and key holding services provide the security needed to enjoy your Mediterranean home without worry.

Having a reliable local partner ensures your property remains in peak condition and complies with all local regulations. Whether it’s managing utility payments or conducting regular security checks, professional asset care maintains the long-term value of your Spanish villa or apartment.

We invite you to contact our team at KEYS property group for a personalized consultation. Let us help you navigate the complexities of getting a mortgage in Spain as a non-resident and turn your vision of a Spanish lifestyle into a secure reality.

Your Mediterranean Future Starts with Professional Strategy

Getting a mortgage in Spain as a non-resident in 2026 is a methodical journey that rewards early preparation and specialized expertise. You’ve now seen how to navigate the specific LTV limits for international buyers and the importance of aligning your financial timeline with Spanish legal milestones.

Success lies in presenting a high-quality solvency profile that builds immediate trust with local lenders. By coordinating your mortgage application with professional legal oversight, you ensure that every stage of the acquisition is transparent, secure, and tailored to your long-term lifestyle goals.

At KEYS property group, we bring over 20 years of local expertise to your property search and financing. Our team provides integrated legal and financial support, followed by dedicated post-sale key holding and maintenance to protect your investment while you’re abroad. We act as your knowledgeable bridge to a seamless transition.

Secure your Spanish property with expert mortgage facilitation from KEYS property group. Your new life in the sun is within reach, and we’re here to ensure you step into it with absolute confidence and professional assurance.

Frequently Asked Questions

What is the maximum LTV for a non-resident mortgage in Spain?

The maximum Loan-to-Value (LTV) for EU residents is 70%, while non-EU residents are typically capped at 60%. These limits are strictly based on the lower of the purchase price or the bank’s official property valuation.

You should prepare a larger initial deposit to cover the remaining balance and the necessary acquisition costs. This ensures a stable equity position from day one of your investment.

Do I need a Spanish bank account to get a mortgage?

You absolutely need a Spanish bank account to service your loan installments and manage property expenses. Lenders require a local account for the direct debit of monthly repayments and mandatory home insurance premiums.

This account also serves as the primary hub for managing your property’s utility bills and community fees. Establishing this account early demonstrates your commitment to the Spanish banking system.

How long does the mortgage application process take for foreigners?

The mortgage application journey generally takes between 8 and 12 weeks from the initial inquiry to final completion. This timeframe includes the property appraisal, the bank’s risk assessment, and the mandatory 10-day reflection period required by law.

Coordination between your legal team and the bank is essential to meeting your property completion deadlines. Professional facilitation can help streamline these steps to avoid administrative delays.

Can I get a mortgage in Spain if I am retired?

Spanish banks do lend to retirees who can demonstrate a stable and verified pension income from their home country. The primary restriction is the age limit, as most lenders require the loan to be fully repaid by the time you reach 75.

This may result in a shorter mortgage term and higher monthly repayments compared to younger applicants. It remains a viable path for those seeking a Mediterranean lifestyle.

What are the typical closing costs for a property with a mortgage?

You should budget for closing costs ranging from 12% to 15% of the property’s purchase price to cover taxes and fees. These funds cover essential expenses such as Transfer Tax (ITP), Notary fees, and Land Registry charges.

These costs are not covered by the mortgage and must be available in your Spanish account before completion. Proper financial planning ensures that these administrative requirements don’t interrupt your purchase timeline.

Is it possible to apply for a Spanish mortgage remotely?

Getting a mortgage in Spain as a non-resident can be managed almost entirely remotely through modern digital banking portals. You can submit your financial documentation and track your application’s progress from your home country with ease.

For the final signing at the notary, you can appoint a representative via power of attorney if you cannot travel to Spain. This digital-first approach offers significant flexibility for global investors.

What is an NIE number and why do I need it for my mortgage?

An NIE (Número de Identidad de Extranjero) is your mandatory tax identification number for all legal and financial dealings in Spain. You cannot open a bank account, sign a mortgage deed, or pay property taxes without this unique identifier.

It’s a critical document that should be secured at the very beginning of your property acquisition journey. Our team at KEYS property group can assist you in obtaining this number to ensure your process stays on track.

Should I choose a fixed or variable rate mortgage in 2026?

In 2026, fixed rates provide peace of mind against market fluctuations, while variable rates offer lower initial costs for those with a higher risk tolerance. Mixed mortgages have become a popular middle ground, offering a fixed rate for the first few years.

Your choice should align with your long-term financial strategy and your specific plans for early repayment. Professional advice can help you weigh these options effectively.

Properties in Getting a Mortgage in Spain as a Non-Resident: The 2026 Essential Guide