How to Transfer Money from Spain After Selling Property: The 2026 Financial Guide

Did you know that transferring €200,000 through a traditional bank could cost you upwards of €6,000 in hidden exchange rate margins alone? While the successful sale of your Spanish villa is a moment for celebration, many owners find the final step of repatriating their wealth to be the most stressful. Learning how to transfer money from Spain after selling property requires more than a simple click of a button; it demands a strategic approach to preserve your hard-earned equity.

It’s natural to feel overwhelmed by the sudden shift from lifestyle dreams to the technical realities of Spanish tax law and banking reporting rules. You deserve a transition that’s as smooth and sophisticated as the property you just sold. We’ll help you master the intricacies of the 19% capital gains tax and the 3% non-resident retention while ensuring full compliance with 2026 financial regulations.

This guide provides a clear roadmap through the latest international transfer thresholds and currency optimization strategies. You’ll discover how to minimize bank commissions and secure a predictable final amount in your home currency.

Key Takeaways

- Master the most sophisticated strategies for how to transfer money from Spain after selling property to ensure your equity remains protected.

- Navigate the nuances of the 3% non-resident retention and ensure your documentation is perfectly aligned for an effortless wealth transition.

- Learn how to utilize forward contracts to shield your property proceeds from the unpredictable nature of global currency volatility.

- Compare the distinct advantages of bespoke currency exchange services over traditional banks to maximize the final value of your transaction.

- Align your financial transition with expert legal assistance to ensure an elegant and secure conclusion to your property journey.

The Financial Landscape of Post-Sale Transfers in Spain

The moment the notary’s ink dries on your deed marks the beginning of a vital financial transition. Successfully closing your sale is only half the journey; the true measure of your success lies in how you repatriate those proceeds. This phase is the “last mile” of your investment where precision and timing become your most valuable assets.

Understanding how to transfer money from Spain after selling property is essential for protecting your final ROI. Since January 2026, the Spanish central bank has tightened its oversight on large capital movements to ensure transparency. Any international transfer exceeding €10,000 triggers a reporting requirement within the Spanish tax system to verify the origin of funds.

Moving your wealth from Euro into your home currency involves more than a simple bank wire. It requires a sophisticated strategy to ensure your life-changing capital arrives intact and ready for its next purpose. Without a plan, you risk seeing your hard-earned equity diminished by avoidable fees and unfavorable market shifts.

Understanding the Scale of the Transaction

Property transactions involve sums that far exceed daily spending limits, triggering enhanced security protocols across the European banking network. These measures aren’t just bureaucratic hurdles; they’re essential safeguards designed to protect your significant assets during transit. We treat these movements with the gravity they deserve, ensuring every protocol is met with meticulous care.

Moving a lifetime of equity across borders is often an emotional experience for our clients. It represents the closing of a vibrant chapter in Spain and the opening of new opportunities elsewhere. This transition requires a trusted guide who respects the personal significance of your financial legacy.

Common Pitfalls of Traditional Spanish Banking

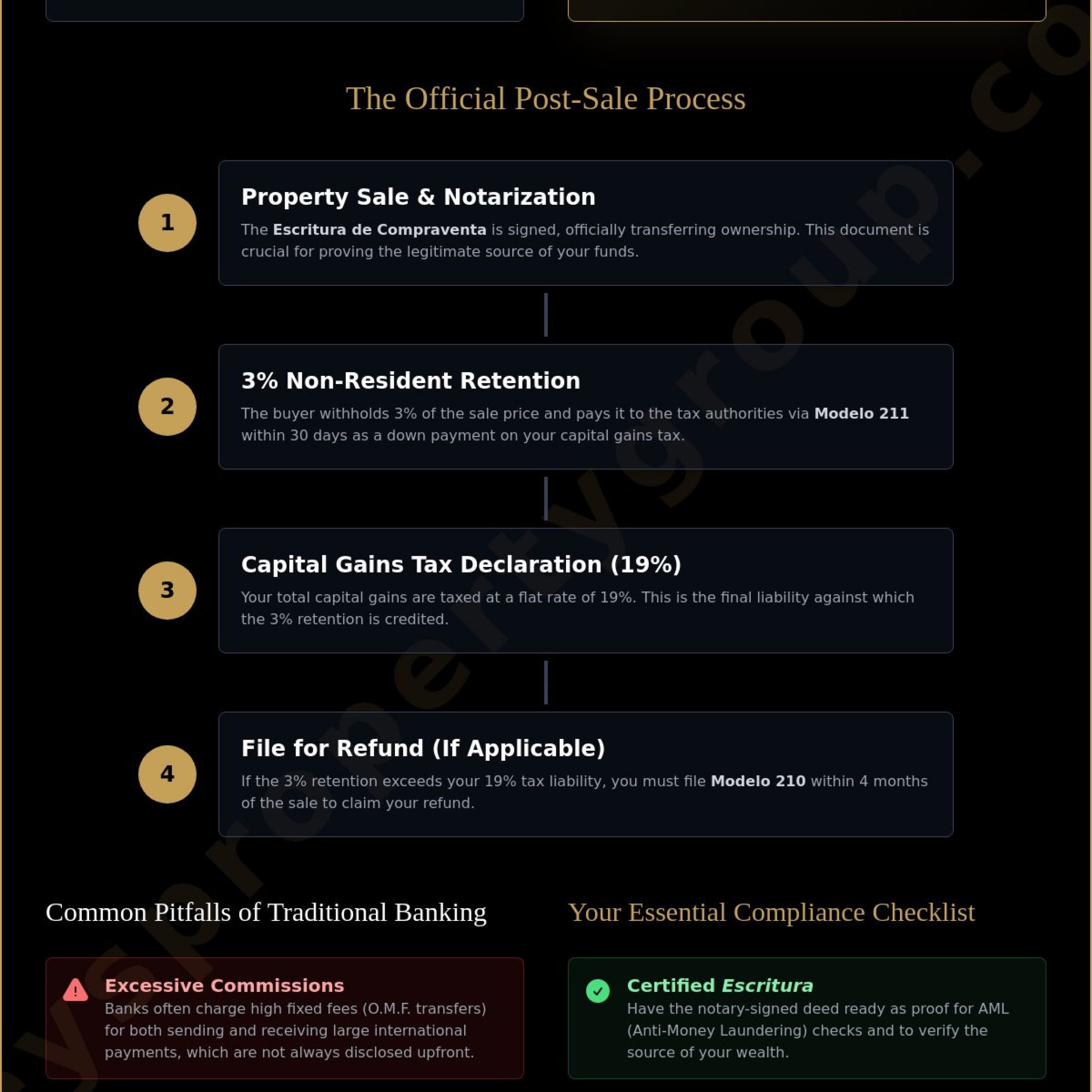

High-street banks in Spain often apply significant commissions for both receiving and sending large sums. These charges, sometimes categorized as O.M.F. transfers, can surprise sellers who haven’t negotiated their terms well in advance. It’s common for these institutions to prioritize their own margins over your final proceeds.

Spain’s unique “bank cheque” culture often creates a temporary liquidity gap that can be frustrating. These physical documents must be cleared through the system, which can delay the final transfer of your funds by several business days. Managing this timeline is crucial if you have immediate plans for your capital in your home country.

Relying on standard retail exchange rates is a frequent mistake that leads to unnecessary losses. Without a dedicated strategy, you might lose thousands of Euros simply by accepting a bank’s daily “off-the-shelf” rate. We believe your wealth deserves the protection of professional currency management rather than the convenience of retail banking.

Essential Tax and Legal Obligations for Sellers

Selling a luxury villa or penthouse is a life-changing transition, but the Spanish Tax Agency ensures it remains a strictly regulated one. Before you can finalize how to transfer money from Spain after selling property, you must address the non-resident retention. This 3% withholding is a legal mandate where the buyer pays a portion of your sale price directly to the authorities as a guarantee against your future taxes.

The Escritura de Compraventa serves as the definitive proof of your transaction’s legitimacy. Spanish banks and international currency providers require this notary-signed document to authorize the release of your proceeds. Without a certified copy of the Escritura, your funds may remain locked in a Spanish account while authorities verify the source of wealth.

Maintaining an active Spanish bank account for several months post-sale is a strategic necessity. This allows for the seamless settlement of final utility bills and the eventual receipt of any tax refunds you may be owed. Our legal assistance team ensures these final details are handled with the precision your portfolio deserves.

The 3% Retention and Refund Process

The buyer submits the 3% withholding using Modelo 211 within 30 days of the sale date. If your actual capital gains tax liability is lower than this amount, you’re entitled to claim a refund via Modelo 210. You have exactly four months from the sale to file this declaration and begin the recovery process.

Success in reclaiming these funds depends on meticulous record-keeping of your original purchase price and renovation costs. When evaluating the most efficient route for your capital, Comparing the Best Methods for International Fund Transfers can provide valuable perspective on digital versus traditional options. Digital platforms often offer the transparency needed for these high-value movements.

Anti-Money Laundering (AML) Compliance

Modern banking regulations require exhaustive “Source of Wealth” evidence for any international transfer exceeding €10,000. Your receiving bank will scrutinize the sale contract to ensure total transparency and compliance with 2026 reporting standards.

Prepare your documentation early to prevent frustrating delays in your wealth transition. Having a clear audit trail from the notary’s office to your home bank ensures your capital remains accessible and secure.

Comparing the Best Methods for International Fund Transfers

Choosing the right vehicle for your wealth is as critical as the property sale itself. When deciding how to transfer money from Spain after selling property, you must weigh the security of traditional institutions against the efficiency of modern financial specialists. A well-chosen method ensures that your life-changing capital arrives at its destination with its value fully preserved.

Every global destination carries its own set of regulatory hurdles, whether you’re repatriating funds to the United Kingdom, the United States, or across the Eurozone. You need a solution that balances speed with the meticulous transparency required by modern anti-money laundering standards. Your strategy should prioritize the protection of your equity above simple convenience.

Why Banks Often Charge More

Traditional high-street banks often rely on the familiarity of their existing relationship with you to justify higher costs. They rarely offer the interbank rate, instead applying an exchange rate margin that can range from 2% to 5% of your total capital. On a €500,000 villa sale, this spread alone could cost you €25,000 in lost value.

Spanish banks frequently impose additional administrative fees for processing the bank cheques used during the completion at the notary. These processing charges, often between €20 and €75, are small but indicative of a system that prioritizes institutional profit. Banks lack the agility to provide the bespoke timing needed for large-scale property transfers.

The “hidden” cost of bank transfers is often found in the lack of transparency regarding the final amount received. Without a fixed rate, you’re at the mercy of the market at the exact moment the bank decides to process your wire. This unpredictability is a risk that sophisticated sellers simply don’t need to take.

The Benefits of a Dedicated Currency Specialist

A specialist currency broker offers a boutique experience that aligns perfectly with the needs of high-net-worth individuals. They provide a personal advisor who monitors market volatility on your behalf, ensuring you execute your exchange at the most opportune moment. This level of care transforms a standard transaction into a strategic financial move.

One of the most powerful tools in your arsenal is the forward contract. This allows you to lock in a favorable exchange rate for up to a year in advance, providing absolute certainty for your future budget. It’s an essential shield against the currency fluctuations that often occur during the weeks between the initial deposit and the final signing.

Digital transfer platforms have also become a viable option, particularly for smaller secondary payments or settling final tax obligations. For a transfer of €30,000, these services might charge as little as €150, offering a transparent alternative to retail banking. However, for six-figure property proceeds, the personalized security of a dedicated broker remains the gold standard.

Strategic Steps to Optimizing Your Currency Exchange

The transition from the notary’s office to the final transfer of your wealth requires a blend of foresight and agility. To truly master how to transfer money from Spain after selling property, you must move beyond passive observation and into active currency management. This strategic phase ensures that the luxury value you’ve built in your home is reflected in your bank balance abroad.

A forward contract acts as a sophisticated anchor in an often turbulent sea of exchange rate fluctuations. By securing a rate at the moment you sign your deposit agreement, you eliminate the anxiety of watching your proceeds potentially dwindle during the completion period. This level of certainty is the hallmark of a well-managed property exit.

Limit orders allow you to set an aspirational target for your exchange rate, triggering an automatic purchase only when the market hits your desired peak. This proactive approach ensures you never miss a favorable spike in value while you focus on your next transition. Coordinating these financial movements with your legal assistance team is paramount to ensuring funds are released the moment the deed is signed.

Timing the Market Effectively

The economic landscape of 2026 presents a unique set of variables, from shifting European interest rates to evolving trade agreements that sway the Euro’s strength. Waiting until the morning of your completion to check the exchange rate is a gamble that rarely favors the seller. You deserve a more refined approach that respects the scale of your investment.

Fluid market conditions can shift the value of a villa sale by thousands of Euros in a single afternoon. By monitoring volatility in the weeks leading up to your appointment, you gain the perspective needed to make an informed decision. Professional guidance during this window turns market movement into an opportunity rather than a risk.

Managing the Spanish Bank Exit

Closing your Spanish chapter involves more than just a wire transfer; it requires a clean exit from the local banking system. Negotiating the cancellation fees for your account in advance ensures that no small, lingering charges disrupt your final balance. Clear communication with your bank manager helps avoid the “exit commissions” that some institutions attempt to levy on departing clients.

For transfers within the Eurozone, SEPA offers an elegant, cost-effective solution for moving your wealth with remarkable speed. However, if your journey takes you beyond Europe, the SWIFT network provides the global reach and security required for significant international capital movements. Understanding the nuances between these systems allows you to choose the path that best preserves your liquidity and peace of mind.

Ensuring a Seamless Wealth Transition with KEYS property group

The sale of a luxury villa or penthouse is a significant milestone, but the true conclusion of the journey occurs when your capital is safely positioned for its next venture. At KEYS property group, we recognize that mastering how to transfer money from Spain after selling property is a vital component of your overall success. Our commitment to your portfolio extends well beyond the physical exchange of keys.

We provide a sophisticated bridge between the Spanish market and your global financial goals. By offering integrated access to our vetted network of specialists, we ensure that every tax obligation and reporting requirement is met with absolute precision. You deserve a partner who views your wealth repatriation with the same level of care as the property marketing itself.

Our boutique approach means you’ll have a dedicated advisor to guide you through the final intricacies of international capital movements. We prioritize transparency and reliability, ensuring you feel both impressed by our expertise and reassured by our personalized care. This holistic view of the transaction allows you to close your Spanish chapter with total confidence.

Our Concierge Approach to Property Sales

We treat the repatriation of your funds as a core priority rather than a secondary concern. Our team connects you with elite legal assistance and currency exchange professionals who possess deep roots in the local landscape. These experts understand the specific rhythms of the Spanish financial system, ensuring your transition is as elegant as the lifestyle you’ve enjoyed here.

You’ll find that our hospitality extends to every facet of the selling process. We’re here to make sure you feel welcomed and supported, even as you prepare for your next international move. Our goal is to transform a complex financial necessity into a smooth, life-changing transition.

Next Steps for Your International Move

Initiating your wealth transition begins with a private consultation with our trusted currency exchange partners. They’ll help you evaluate the current market and determine if a forward contract or limit order aligns with your timing. This proactive step is the most effective way to safeguard your proceeds from the start.

Before your completion date at the notary, ensure you have your “Source of Wealth” documentation ready for your receiving bank. A final checklist for a stress-free fund transfer includes:

- Confirming your fiscal representative has filed all necessary tax forms post-sale.

- Verifying that your Spanish bank account is prepared for the final wire and eventual closure.

- Synchronizing your transfer with the latest 2026 central bank reporting standards.

Success in the Spanish market requires a guide who understands that the financial finish line is just as important as the initial sale. Let KEYS property group help you navigate the final steps of your journey with the exclusivity and care you expect. Your legacy deserves a flawless transition.

Mastering Your Financial Future Beyond the Sale

You’ve navigated the complexities of the Spanish market and successfully closed your property sale. Now, ensuring you understand how to transfer money from Spain after selling property is the final step in protecting your investment’s legacy. By managing tax retentions and exchange rate volatility with precision, you secure the full value of your hard-earned equity.

Our team brings over 20 years of local expertise to every transaction, providing the end-to-end legal and financial support our discerning international clientele expects. We treat your wealth transition with the same boutique care and sophisticated attention that defined your property journey from the very beginning. This commitment ensures your transition is as rewarding as the time you spent in your Spanish home.

Take the next step toward a seamless and secure repatriation of your funds. Secure your equity with the KEYS property group currency exchange service today. We look forward to guiding you through this final, vital chapter with confidence and absolute clarity.

Frequently Asked Questions

How long does it take to transfer money from Spain after a sale?

Most international transfers from a Spanish bank reach their destination within one to three business days. The exact duration depends on whether your funds move through the SEPA network for European accounts or the SWIFT system for global destinations. Utilizing a dedicated currency specialist can often expedite this timeline by ensuring all compliance checks are completed in advance.

Is there a limit on how much money I can transfer out of Spain?

There’s no legal ceiling on the amount of capital you can repatriate to your home country. However, you must comply with reporting requirements for any international transfer exceeding €10,000 to remain in good standing with the Spanish Tax Agency. Providing clear documentation ensures your wealth transition remains uninterrupted and fully transparent.

Can I avoid the 3% retention tax when selling my Spanish property?

The 3% withholding is a mandatory legal obligation for all non-resident sellers, designed as a guarantee for your capital gains tax. While you can’t bypass this requirement, you’re entitled to claim a refund if the withheld amount exceeds your actual tax liability. This recovery process typically begins after you’ve filed your final tax declarations with the help of your legal representative.

What documents will my home bank ask for when I receive the funds?

Your receiving bank will require a certified copy of the Notary-signed sale deed, known as the Escritura de Compraventa. This document provides the essential “Source of Wealth” evidence needed to clear large sums through international anti-money laundering protocols. Having these papers ready prevents your funds from being temporarily held or questioned upon arrival.

Should I open a currency broker account before or after the sale?

You should ideally establish your currency broker account several weeks before your completion date at the Notary. Early preparation allows you to monitor market trends and secure a forward contract to lock in a favorable exchange rate. This proactive approach is the most effective way to protect your equity from sudden market shifts during the closing period.

What are the typical fees for sending a large international transfer from a Spanish bank?

High-street banks in Spain typically charge a processing fee alongside an exchange rate margin that can range from 2% to 5% of the total sum. Mastering how to transfer money from Spain after selling property involves comparing these retail costs against specialist providers who offer much tighter spreads. Choosing the right partner can save you a significant amount on a six-figure villa sale.

Can I transfer my property money directly from the Notary to my home country?

Proceeds are almost always deposited into a Spanish bank account first, as the buyer typically provides a bank cheque at the Notary’s office. Once these funds are cleared in your local account, they can then be moved internationally through your chosen transfer method. Coordinating this step with your legal and financial advisors ensures the capital moves toward its final destination without unnecessary delays.

Properties in How to Transfer Money from Spain After Selling Property: The 2026 Financial Guide